Taiwan Semiconductor Manufacturing Company Ltd (2330.TW) is the world’s largest contract manufacturer of integrated circuits and semiconductors. The service includes wafer manufacturing, probing, assembly and testing, mask production, and design services. [mepr-active membership=”1734″ ifallowed=”show” unauth=”message” unauth_message=”Please login or purchase a membership to view full text.”] With twelve wafer production facilities, Taiwan Semiconductors produced 9m 12-inch equivalent wafers in 2015. The company has a market share of 55% in the global semiconductor foundry segment.

Taiwan Semiconductor Manufacturing Company Ltd (2330.TW) is the world’s largest contract manufacturer of integrated circuits and semiconductors. The service includes wafer manufacturing, probing, assembly and testing, mask production, and design services. [mepr-active membership=”1734″ ifallowed=”show” unauth=”message” unauth_message=”Please login or purchase a membership to view full text.”] With twelve wafer production facilities, Taiwan Semiconductors produced 9m 12-inch equivalent wafers in 2015. The company has a market share of 55% in the global semiconductor foundry segment.

Taiwan Semiconductor served about 470 customers and manufactured nearly 9 thousand products for various applications. Among the clients are Apple and Qualcomm, each accounting for 16% of the company’s revenues, as well as NVIDIA, Huawei, and MediaTek.

Taiwan Semiconductor was founded in 1987 and on in Hsinchu/Taiwan. The company is listed on the Taiwan Stock Exchange since September 1994. It shares can also be traded as ADR in the US, Germany, Argentina, and Mexico.

The semiconductor and electronics industry is a highly cyclical business with significant periods of downturns and overcapacity. The industry’s revenues, earnings, and margins can, therefore, fluctuate significantly. As an upstream supplier in the semiconductor supply chain, chipmakers are highly dependent of the market conditions of the three Cs: communications, computer, consumer, as well as of the emerging Internet-of-Things. However, there are also plenty of growth opportunities with the rising demand of connected or smart devices in electric and self-driving cars, drones, robots, virtual/augmented reality, artificial intelligence, and wearables. All these products require powerful chips with a significant increase in processor speeds and capability.

Taiwan Semiconductor just plans a 500bn TWD ($15.7 billion) facility in Taiwan to manufacture 5nm and 3nm chips to keep an edge over major competitors such as Samsung Electronics and Intel. The smaller the size, the more advanced the chip, but the more challenging the development too. Apple’s iPhone 7 uses Taiwan Semiconductor’s 16nm chips currently.

Taiwan Semiconductor forecasts the industry to grow by 1% only this year, but for more than 3% annually in the upcoming years due to an increasing number of semiconductors in electronic devices, an increase of market share by fabless companies, and a rising demand for Application-Specific Integrated Circuits (ASIC).

With a workforce of more than 45 thousand employees, Taiwan Semiconductor reported revenues of 685.7bn TWD (21.4bn USD) and a profit before tax of 273.9bn TWD (8.5bn USD), an increase of 7.2% and 1.5% respectively for the first nine months of this year. In 2015 revenues and profit were up 11% and 16% respectively. The company had cash and equivalents of 464bn TWD (14.5bn USD) by the end of September. Taiwan Semiconductor has a healthy equity ratio of 75% and a very low gearing ratio. Operating margins are well above industry average.

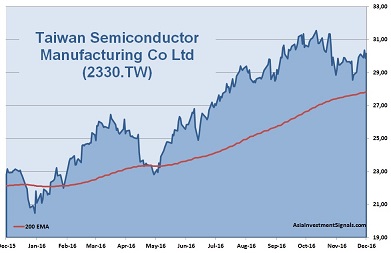

Taiwan Semiconductor’s shares are in a strong uptrend since five years already and gained nearly 30% since the beginning of this year. The company is currently priced at 16 times earnings. 19 out 30 covering analyst recommend the shares as outperformer or as a buy. The demand for Taiwan Semiconductor’s products will highly depend on the global economy. Further growth opportunities for the company may come from the automobile sector and new electronic devices requesting low power consumption. The reasonable valuation could allow the share price to gain another 15-20% within the next six months.

AIS Rating: ★★★★☆

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 Q1-3 Only |

|

|---|---|---|---|---|---|---|

| EPS (TWDcents) | 5.28 | 6.15 | 7.1 | 9.8 | 11.7 | 9 |

| Change | -16% | 16% | 15% | 38% | 19% | 0.2% |

| P/E | P/E SECTOR |

P/B | P/CF | Equity Ratio* |

ROE | Debt/ Equity** |

Div YLD |

|---|---|---|---|---|---|---|---|

| 16 | 19 | 4 | 9 | 75% | 25% | 34% | 3.2% |

* Equity / Total Assets, ** Total Liabilities / Equity

[/mepr-active]