Lion Rock Group Ltd (1127.HK) is one of the world’s leading supplier of print services for book publishers with an annual revenue exceeding 200m USD. The company provides printing services to international book publishers, professional and educational publishing conglomerates, and print media companies.[mepr-active membership=”1734″ ifallowed=”show” unauth=”message” unauth_message=”Please login or purchase a membership to view full text.”] Products include hard back books, paperback books, wire-o binding, saddle stitching, children’s book, board books, and book plus. Lion Rock just recently changed its name from 1010 Printing Group, as it was known before. The company has 27 offices and printing facilities in China, Hong Kong, Singapore, Australia, the US, and in the UK. 37% of Lion Rock’s revenues are generated in Australia, followed by the US (31%) and UK (17%).

Lion Rock Group Ltd (1127.HK) is one of the world’s leading supplier of print services for book publishers with an annual revenue exceeding 200m USD. The company provides printing services to international book publishers, professional and educational publishing conglomerates, and print media companies.[mepr-active membership=”1734″ ifallowed=”show” unauth=”message” unauth_message=”Please login or purchase a membership to view full text.”] Products include hard back books, paperback books, wire-o binding, saddle stitching, children’s book, board books, and book plus. Lion Rock just recently changed its name from 1010 Printing Group, as it was known before. The company has 27 offices and printing facilities in China, Hong Kong, Singapore, Australia, the US, and in the UK. 37% of Lion Rock’s revenues are generated in Australia, followed by the US (31%) and UK (17%).

Lion Rock was founded in 2005 and is headquartered in Hong Kong. The shares are listed on the Main Board of Hong Kong’s Stock Exchange since 2011. Lion Rock’s shares can also be traded in the US. Major shareholder is the executive director, Mr. Lau Chuk Kin, with an ownership of 41%. 38% of the shares are in public hand.

With a workforce of 1,336 employees, Lion Rock reported revenues of 713m HKD (91m USD) and profit before tax of 72m HKD (9m USD) over the first half year 2017. This is a decrease of 11% and 9% respectively compared to the same period a year ago. The decrease was due to more competitive sales pricing, eroding margin, the disposal of its outdoor printing business, and currency effects.

In 2016, revenues decreased already 8% while profits increased 5%. The operating margin of 14% is well above industry average. The company had a comfortable cushion of cash of 444m HKD (57m USD) at the end of June 2017, which could be used to finance further acquisitions. In March, Lion Rock acquired Regent Publishing Services, a publishing service company that is thought to broaden the customer base and to strengthen the purchasing power. Lion Rock shows a solid balance sheet with an equity ratio of 70% and a very low gearing, defined here as total liabilities to total equity, of 42%.

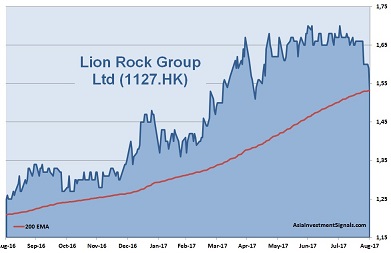

Lion Rock’s shares are in an uptrend since January 2016 and gained more than 60% in value since, 14% alone this year. The stock price peaked in June at 1.7 HKD but lost more than 10% since with the risk of breaking below its 200 moving average line currently. The company is priced at eight times earnings. The shares trade slightly above book value and at three times cash flow only. The last dividend payment yielded almost 5%.

Despite a decline in print revenue, the print market will continue to dominate. Only a quarter of the total income from the newspaper, book, and magazine industries worldwide are forecasted to come from digital publishing by 2020. Even in the US and the UK, two markets with a rapid growth in digital publishing, are expected to have only a share in digital of 42% and 37% respectively by then.

Lion Rock has a leading position in this challenging print publishing industry. Eroding margin, rising labor cost, competition from digital publishing, and recently a sharp increase of paper price will have an adverse impact on the competitive advantage of book printers in China. We believe that Lion Rock is well positioned to face this challenge. Further investments in the print or the digital publishing industry or the acquisition of competitors in key markets are likely. The company is financially stable and comes with a favorable valuation. Despite a deteriorating chart picture, it is worth to keep the company on the watchlist.

AIS Rating: ★★★☆☆

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 H1 only |

|

|---|---|---|---|---|---|---|---|

| EPS (HKDcent) | 14.5 | 11 | 16.7 | 19 | 21.2 | 19 | 6.4 |

| Change | -12% | -24% | 51% | 14% | 11% | -10% | -5% |

| P/E | P/E SECTOR |

P/B | P/CF | Equity Ratio* |

ROE | Debt/ Equity** |

Div YLD |

|---|---|---|---|---|---|---|---|

| 8 | 16 | 1.2 | 3 | 70% | 17% | 42% | 4.9% |

* Equity / Total Assets, ** Total Liabilities / Equity

[/mepr-active]