Xinyi Glass Holdings Limited (0868.HK) is a leading glass manufacturer producing glass products including automobile glass, energy-saving construction glass, high quality float glass and other glass products for different commercial and industrial applications. Xinyi has six production facilities in China and Malaysia. Its products are sold to more than 130 countries, including China, Hong Kong, Australia, New Zealand, Africa, the Middle East, Central and South America. According to company information Xinyi accounts for around 20% of the world automobile glass replacement market and around 15% of the LOW-E energy-conversation glass market.

Xinyi Glass Holdings Limited (0868.HK) is a leading glass manufacturer producing glass products including automobile glass, energy-saving construction glass, high quality float glass and other glass products for different commercial and industrial applications. Xinyi has six production facilities in China and Malaysia. Its products are sold to more than 130 countries, including China, Hong Kong, Australia, New Zealand, Africa, the Middle East, Central and South America. According to company information Xinyi accounts for around 20% of the world automobile glass replacement market and around 15% of the LOW-E energy-conversation glass market.

The Hong Kong based group was founded in 1988 and is listed on the main board of the Hong Kong Stock Exchange since February 2005. The shares can also be traded in the US and in Germany.

Despite a difficult operational environment for construction and float glass due to the slowed down in China’s economy and due to a highly competitive market environment for energy-saving glass, Xinyi was able to grow through productivity improvements and through the use of improved technology and economies of scales in 2015. Xinyi’s solar business will profit from the continuous growth in solar power deployment in China. China and Hong Kong account still for more than 70% of Xinyi’s sales, but the group implements aggressive marketing strategies to introduce new products and to approach new overseas customers.

With a staff of 12,746 people Xinyi generated revenues of 11.5bn HKD and net profits of 2.1bn HKD in 2015, an increase of 5.5% and 55% respectively compared to the year ago. The net profit margin of 18% is well above industry average. Xinyi holds cash reserves of 1.3bn HKD by the end of 2015 and is well positioned to explore new overseas opportunities. The group has just announced a positive profit alert for the six months period ending June 2016. Cost reduction and higher sales in the float glass business as well as an increase in profits in its solar business is expected to boost net profit by 30% to 45% compared to the same period a year ago. The company is currently prices at 11 times its earning and comes with a dividend yield of 4.5%.

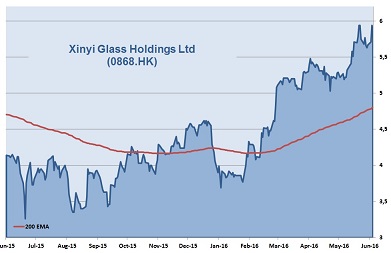

From eight covering analysts, all see the company as outperformer or a buy with a share price target of up to 7 HKD. We like the low valuation, the good profitability and the financial strength of the company and expect further growth opportunities from overseas expansions. The stock is trending since February and could, with some tailwind from a further stable demand in the construction and solar industry, reach old highs at above 8 HKD in the next 12 months, an upside potential of more than 40%.

AIS Rating: ★★★★☆

| 2012 | 2013 | 2014 | 2015 | 2016E | |

|---|---|---|---|---|---|

| EPS (HKD cents) | 31.4 | 89.1 | 34.57 | 53.11 | 61.57 |

| Change | -10% | 184% | -61% | 54% | 16% |

| P/E | P/E Industry |

P/B | P/CF | Equity Ratio |

ROE | Debt/ Equity |

Div YLD |

|---|---|---|---|---|---|---|---|

| 11 | 18 | 1.8 | 8 | 59% | 17% | 47% | 4.5% |