PT Indal Aluminium Industry Tbk (INAI.JK) is one of the largest and most integrated aluminum manufacturer in South East Asia. The Surabaya /Indonesia-based company was founded in 1971 and listed on Jakarta’s Stock Exchange since 1994. Indal is part of the Maspion Group, one of the world largest consumer durable good producer.

PT Indal Aluminium Industry Tbk (INAI.JK) is one of the largest and most integrated aluminum manufacturer in South East Asia. The Surabaya /Indonesia-based company was founded in 1971 and listed on Jakarta’s Stock Exchange since 1994. Indal is part of the Maspion Group, one of the world largest consumer durable good producer.

Indal’s main business activity involves processing aluminum ingot into aluminum extrusion profiles, which are used in construction, in electronic and automotive components, and in household appliances. Indal is furthermore trading aluminum products and is investing in companies in the aluminum and coating industry. 76% of the company’s products are sold to the domestic market followed by 11% to the US market.

Despite a challenging economy and a declining aluminum prices, Indal has boosted sales almost 50% during 2015. Sales in Indal’s contracting services grew strongly as a result of a dynamic development of Indonesia’s infrastructure. Export sales increased by more than 7% in 2015 and another 5% since beginning of 2016 as a result of changes in trade policies in US and China. But also investments in production technology have helped Indal to improve product quality and to better compete globally.

With a staff of more than 2,200 employees, Indal generated record high sales revenues of 1.38tr IDR (105m USD) and a profit before taxes of 57.1bn IDR (4.4m USD) in 2015. Nevertheless, gross profit margins of 12% remain behind industry average. Cost control and productivity-enhancing programs might further improve Indal’s profitability in the near future. The company has also benefited from higher selling prices from old contracts while raw material costs have declined in 2015. For the first half year of 2016 Indal reports sales of 616bn IDR (47m USD) with a profit of 30bn IDR (2.3m USD), an increase of 1.4% and 22.4% respectively compared to the same period a year ago.

The company is highly leveraged with liabilities exceeding equity by more than 4 times. An equity ratio of only 20% shows also some risks in the balance sheet. Cash and cash equivalents have decreased by 25bn IDR this year to 77bn IDR (5.9m USD) mainly due to investing activities.

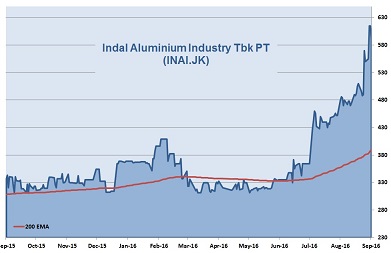

Indal’s stock gained around 46% this year with a strong momentum since June. The company is currently priced at only 6 times its earnings, well below industry average. Noteworthy is the high dividend yield of more than 7%. The stock could improve another 20% in the next six month with the tailwind from a continuous high demand for construction materials in Indonesia and a recovering economy in China.

AIS Rating: ★★★☆☆

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 H1 only |

|

|---|---|---|---|---|---|---|

| EPS (IDR) | 83.2 | 73.1 | 15.8 | 70.8 | 90.3 | 61.6 |

| Change | 66% | -12% | -78% | 347% | 28% | 40% |

| P/E | P/E Industry |

P/B | P/CF | Equity Ratio |

ROE | Debt/ Equity |

Div YLD |

|---|---|---|---|---|---|---|---|

| 6 | 23 | 0.8 | 4.1 | 20% | 16% | 455% | 7.3% |