Boyaa Interactive International Ltd. (0434.HK) is a leading developer of web-based and mobile games in China. The company has more than 600m cumulative registered players in around 100 countries and regions. Its games are available in up to 21 different languages. Boyaa has developed more than 40 online games. Most of them are long-lifespan classic card and board games, such as Texas Hold’em, Fight the Landlord, Boyaa Card Games (Smart TV game) and Sichuan Mahjong. Boyaa’s two most popular games, Texas Hold’em Series and Fight the Landlord, account for more than 85% of the revenues. The Hong Kong based company with an office in Shenzhen was founded in 2000 and went public in November 2013. Its shares can be traded in Hong Kong, the US and in Germany.

Boyaa Interactive International Ltd. (0434.HK) is a leading developer of web-based and mobile games in China. The company has more than 600m cumulative registered players in around 100 countries and regions. Its games are available in up to 21 different languages. Boyaa has developed more than 40 online games. Most of them are long-lifespan classic card and board games, such as Texas Hold’em, Fight the Landlord, Boyaa Card Games (Smart TV game) and Sichuan Mahjong. Boyaa’s two most popular games, Texas Hold’em Series and Fight the Landlord, account for more than 85% of the revenues. The Hong Kong based company with an office in Shenzhen was founded in 2000 and went public in November 2013. Its shares can be traded in Hong Kong, the US and in Germany.

The global gaming market is predicted to generate almost 100bn USD in revenues in 2016, an increase of 8.5% compared to 2015. Mobile gaming, with expected revenues of 36.9bn USD, will increase more than 21%, and surpass PC gaming. China accounts for almost 25% of all global game revenues. Newzoo expects the global market to continue growing at an average rate of 6.6% until 2019, with revenues reaching 119bn USD. Mobile gaming is expected to reach 52.5bn USD by then.

Compared to consoles and PC games where the development and marketing can cost tens of millions of dollars and can take several years to produce, the mobile gaming market has relatively low barriers to entry and is therefore highly competitive. Deloitte estimated more than 800,000 mobile games in app stores beginning of 2016 with 500 new titles launched every day. This compared to only 17,000 titles available for consoles and PCs.

In order to stick out of the crowd, Boyaa organizes online and offline activities and competitions such as its popular Poker Tournament. The company collaborates furthermore closely with large-scale social platforms such as Facebook and Google as well as three large domestic telecom operators. Boyaa also prepares to enter the emerging TV games market by developing high-quality products and by building up close ties with top domestic TV games manufacturers.

With a staff of 836 employees, Boyaa generated revenues of 351m RMB (52.6m USD) and a profit before tax of 149m RMB (22.3m USD) during the first six months of 2016. While revenues decreased by almost 20%, profits improved by more than 80% compared to the same period a year ago. Already in 2015, Boyaa reported shrinking revenues by 14% compared to the year before where revenues peaked at almost 1bn RMB (149.9m USD). The decline is due to the downward trend for the web-based games and to regulation adjustments for SMS payments in China.

Boyaa finances its operations through cash flow and through net proceeds from its IPO. The company has cash reserves of 1.25bn RMB (187m USD) and a cash flow for the first six months of 176m RMB (26m USD). Expansion, investments, and business operations are intended to be financed with internal resources and through organic growth in the future. The company has currently an equity ratio of 88% and basically no debts.

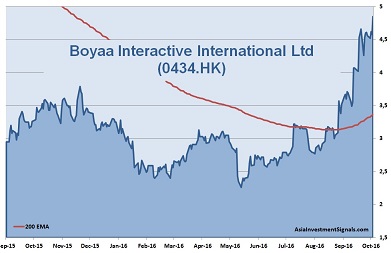

Boyaa’s shares fall to a low of 2.23 HKD in May after the chairman and controlling shareholder has been detained for private reasons for an investigation by judicial authority in the PRC. Since then the shares bounced back and doubled in value. The company is moderately priced at only 7 times its earnings. Earnings per share grew at an average by 23% over the last five years.

Game development is a risky business as the next competitor with a better and trendier product is just around the corner. But we think Boyaa is well positioned with a large portfolio of games and with sufficient funds to market its products and to purchase smaller competitors. We expect also a strong tailwind from its second Poker Tournament this month, with a prize pool of 520,000 USD and 35bn in game chips, which will raise brand awareness and enhance player’s loyalty. Last year’s Poker Tournament attracted more than 2.2m players from all over the world.

AIS Rating: ★★★☆☆

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 H1 only |

|

|---|---|---|---|---|---|---|

| EPS (RMBcents) | n/a | 30.9 | 25.5 | 38.1 | 49.3 | 18 |

| Change | -17% | 49% | 29% | 79% |

| P/E | P/E SECTOR |

P/B | P/CF | Equity Ratio* |

ROE | Debt/ Equity** |

Div YLD |

|---|---|---|---|---|---|---|---|

| 7 | 18 | 1.6 | 7.1 | 88% | 24% | 14% | 3.3% |

* Equity / Total Assets, ** Total Liabilities / Equity