Tat Seng Packaging Group Ltd (T12.SI) value has increased 50% since our first recommendation last year in June. The manufacturer of corrugated paper products and packaging is also part of our model portfolio. With a market cap of 70m USD, Tat Seng Packaging is only a relatively small player. However, the well-managed company has consistently surprised with positive results over the past five years and shows strong financials. EPS grew by 27% over the last five years, a rate well above industry average.[mepr-active membership=”1734″ ifallowed=”show” unauth=”message” unauth_message=”Please login or purchase a membership to view full text.”]

Tat Seng Packaging Group Ltd (T12.SI) value has increased 50% since our first recommendation last year in June. The manufacturer of corrugated paper products and packaging is also part of our model portfolio. With a market cap of 70m USD, Tat Seng Packaging is only a relatively small player. However, the well-managed company has consistently surprised with positive results over the past five years and shows strong financials. EPS grew by 27% over the last five years, a rate well above industry average.[mepr-active membership=”1734″ ifallowed=”show” unauth=”message” unauth_message=”Please login or purchase a membership to view full text.”]

Despite flat revenues, the company has potential to increase its value by improving productivity and leveraging existing business operations. The operating margin of 9.8% lacks behind its industry peers and has room for improvements. The development of new market niches, the acquisition of competitors, or the expansion outside of Singapore and China could be possible scenarios. Tat Seng Packaging had cash reserves of 41m SGD (30m USD) at the end of 2016.

According to Market Research Company Smithers Pira, the annual growth rate of the global packaging industry is estimated at 3.5% until 2020, with sales reaching 997bn USD by 2020. Paper boards make up around one-third of the sectors’ market volume. Especially e-commerce has driven the recent growth in the board packaging industry with a focus on tailoring board packaging to maximize the end-user experience.

With a workforce of 428 employees, Tat Seng Packaging reported revenues of 229m SGD (165m USD) and a profit before tax of 22m SGD (16m USD) for 2016, a slight decrease of 1.3% in revenues, but a record growth of 24.5% in profits compared to the year ago. In 2015, revenues and profits were up 3.1% and 28.3% respectively compared to the year before. The company shows a solid balance sheet with an equity ratio of 47% and a gearing, defined here as total liabilities to total equity, of 114%.

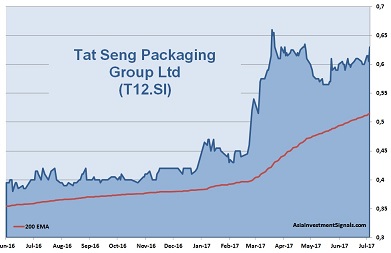

Tat Seng Packaging’s shares are in an uptrend since February 2012 and gained 270% in value since, 54% alone this year. The company is currently priced at only seven times earnings, compared to 36 times among its sector peers. The shares trade below book value and at four times cash flow only. The last dividend payment yielded 5%. On a five year annualized basis, dividend per share growth ranked highest among its industry peers.

Read also: Tat Seng Packaging – A Company Warren Buffett Would Like

AIS Rating: ★★★★☆

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | |

|---|---|---|---|---|---|---|

| EPS (SGD) | 0.03 | 0.05 | 0.08 | 0.06 | 0.08 | 0.09 |

| Change | -25% | 67% | 60% | -25% | 33% | 13% |

| P/E | P/E SECTOR |

P/B | P/CF | Equity Ratio* |

ROE | Debt/ Equity** |

Div YLD |

|---|---|---|---|---|---|---|---|

| 7 | 36 | 0.9 | 4 | 47% | 14% | 114% | 5% |

* Equity / Total Assets, ** Total Liabilities / Equity

[/mepr-active]