Valuetronics Holdings Ltd (BN2.SI) is a premier electronic manufacturing service provider for some of the world’s leading brands in consumer electronics and industrial and commercial electronics. Valuetronics designs and manufactures products such as printers, temperature sensing devices, communication and GPS products, data and media connectivity modules for cars, medical diagnostic equipment, as well as consumer lifestyle and smart lighting products with IoT features.[mepr-active membership=”1734″ ifallowed=”show” unauth=”message” unauth_message=”Please login or purchase a membership to view full text.”]

Valuetronics Holdings Ltd (BN2.SI) is a premier electronic manufacturing service provider for some of the world’s leading brands in consumer electronics and industrial and commercial electronics. Valuetronics designs and manufactures products such as printers, temperature sensing devices, communication and GPS products, data and media connectivity modules for cars, medical diagnostic equipment, as well as consumer lifestyle and smart lighting products with IoT features.[mepr-active membership=”1734″ ifallowed=”show” unauth=”message” unauth_message=”Please login or purchase a membership to view full text.”]

Valuetronics is currently one of only two suppliers for the second generation smart light LEDs, and well positioned to benefit from the third generation too. The company has its manufacturing facility located in the Guangdong Province, China. In 2005, Valuetronics became the preferred supplier for consumer lifestyle products of Philips, the Dutch electronics giant and biggest lighting company in the world. Later it also became its preferred supplier for lighting products. Currently, four major customers make up for around 70 percent of Valuetronics’ revenues. The US market accounts for almost half of the company’s revenue, followed by China with roughly a third of the revenues.

Valuetronics was founded in 1992 and is headquartered in Hong Kong. The shares are listed on the main board of Singapore’s stock exchange since 2007, but can also be traded in Germany and the US. Major shareholders are the two directors, Tse Chong Hing and Chow Kok Kit, with an ownership of together 26 percent. 72 percent of the shares are in public hand.

With a workforce of around 4,000 employees, Valuetronics reported revenues of 2.2bn HKD (282m USD) and profits before tax of 180m HKD (23m USD) over the first nine months of the fiscal year 2017/18. This is an increase of 35 and 43 percent respectively compared to the same period a year ago. Especially the consumer electronics business grew by 48 percent on increased demand for consumer lifestyle and smart LED lighting products with IoT features. The industrial and commercial electronics business grew by 22 percent on higher demand for printers and in-car connectivity modules used in the automotive industry. In the fiscal year 2016/17, Valuetronics’ revenues and profits increased by 17 and 28 percent respectively. The operating margin of 8 percent remains below industry average and need improvements.

Valuetronics had 640m HKD (82m USD) in cash at the end of 2017 and managed to maintain zero bank borrowings over the last five years already. The company shows a solid balance sheet with satisfactory profitability and good financial strength. The equity ratio is at 47 percent and the gearing, defined here as total liabilities to total equity, at 111 percent. Next earning results will be announced on 25.May.

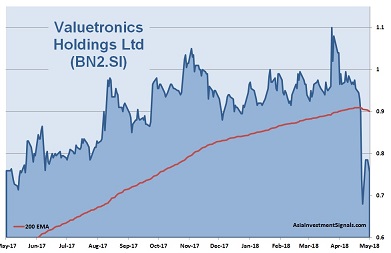

Valuetronics’ shares increased by more than 18 times since 2009 and peaked in March. Since then, the shares lost more than 30 percent in value. The strong decline was to a large extent the reaction to Valuetronics’ major customer Philips, who reported a weak first-quarter result of its home segment, notably in the US. But Philips’ management expects sales to normalize and maintains its full-year target of double-digit growth. The management reassured that the positive structural trend for smart home lighting remains intact. However, weak earnings at Valuetronics’ competitors as well as a soft sentiment in the electronics and semiconductor sector caused further uncertainties.

The strong decline sent Valuetronics’ valuation back to 9 times earnings. The shares trade about twice the book value and at 13 times operating cash flow. The latest dividend yielded almost 5 percent. The majority of covering analysts rate the stock still as an outperformer.

Valuetronics shows a robust balance sheet. The valuation is back to levels worth buying. The industry outlook remains positive. Valuetronics will benefit from the fast-growing segment of in-car connectivity modules as well as from the trend to home products with IoT features. Market penetration of smart home lighting outside the US is very still low. The company is well positioned in a strong competitive environment. We expect deals with new customers to be announced soon. Assuming a stable global economy, the share price could reach again levels above 1 SGD by the end of this year.

AIS Rating: ★★★★☆

| 2012/13 | 2013/14 | 2014/15 | 2015/16 | 2016/17 | 2017/18 Q1-3 Only |

|

|---|---|---|---|---|---|---|

| EPS (HKDcents) | 22 | 40 | 40 | 29 | 37 | 37 |

| Change | -40% | 85% | -1% | -28% | 27% | 40% |

| P/E | P/E SECTOR |

P/B | P/CF | Equity Ratio* |

ROE | LIAB./ Equity** |

Div YLD |

|---|---|---|---|---|---|---|---|

| 9 | 13 | 1.9 | 13 | 47% | 20% | 111% | 5% |

* Equity / Total Assets, ** Total Liabilities / Equity

[/mepr-active]